A popular and widely used statistical method for time series forecasting is the ARIMA model.

ARIMA stands for AutoRegressive Integrated Moving Average and represents a cornerstone in time series forecasting. It is a statistical method that has gained immense popularity due to its efficacy in handling various standard temporal structures present in time series data.

In this tutorial, you will discover how to develop an ARIMA model for time series forecasting in Python.

After completing this tutorial, you will know:

About the ARIMA model the parameters used and assumptions made by the model.

How to fit an ARIMA model to data and use it to make forecasts.

How to configure the ARIMA model on your time series problem.

Kick-start your project with my new book Time Series Forecasting With Python, including step-by-step tutorials and the Python source code files for all examples.

Let’s get started.

Updated Apr/2019: Updated the link to dataset.

Updated Sep/2019: Updated examples to use latest API.

Updated Dec/2020: Updated examples to use latest API.

Updated Nov/2023: #####

Autoregressive Integrated Moving Average Model

The ARIMA (AutoRegressive Integrated Moving Average) model stands as a statistical powerhouse for analyzing and forecasting time series data.

It explicitly caters to a suite of standard structures in time series data, and as such provides a simple yet powerful method for making skillful time series forecasts.

ARIMA is an acronym that stands for AutoRegressive Integrated Moving Average. It is a generalization of the simpler AutoRegressive Moving Average and adds the notion of integration.

Let’s decode the essence of ARIMA:

AR (Autoregression): This emphasizes the dependent relationship between an observation and its preceding or ‘lagged’ observations.

I (Integrated): To achieve a stationary time series, one that doesn’t exhibit trend or seasonality, differencing is applied. It typically involves subtracting an observation from its preceding observation.

MA (Moving Average): This component zeroes in on the relationship between an observation and the residual error from a moving average model based on lagged observations.

Each of these components is explicitly specified in the model as a parameter. A standard notation is used for ARIMA(p,d,q) where the parameters are substituted with integer values to quickly indicate the specific ARIMA model being used.

The parameters of the ARIMA model are defined as follows:

p: The lag order, representing the number of lag observations incorporated in the model.

d: Degree of differencing, denoting the number of times raw observations undergo differencing.

q: Order of moving average, indicating the size of the moving average window.

A linear regression model is constructed including the specified number and type of terms, and the data is prepared by a degree of differencing to make it stationary, i.e. to remove trend and seasonal structures that negatively affect the regression model.

Interestingly, any of these parameters can be set to 0. Such configurations enable the ARIMA model to mimic the functions of simpler models like ARMA, AR, I, or MA.

Adopting an ARIMA model for a time series assumes that the underlying process that generated the observations is an ARIMA process. This may seem obvious but helps to motivate the need to confirm the assumptions of the model in the raw observations and the residual errors of forecasts from the model.

Next, let’s take a look at how we can use the ARIMA model in Python. We will start with loading a simple univariate time series.

Stop learning Time Series Forecasting the slow way!

Take my free 7-day email course and discover how to get started (with sample code).

Click to sign-up and also get a free PDF Ebook version of the course.

Shampoo Sales Dataset

The Shampoo Sales dataset provides a snapshot of monthly shampoo sales spanning three years, resulting in 36 observations. Each observation is a sales count. The genesis of this dataset is attributed to Makridakis, Wheelwright, and Hyndman (1998).

Save it to your current working directory with the filename “shampoo-sales.csv”.

Loading and Visualizing the Dataset:

Below is an example of loading the Shampoo Sales dataset with Pandas with a custom function to parse the date-time field. The dataset is baselined in an arbitrary year, in this case 1900.

When executed, this code snippet will display the initial five dataset entries:

1

2

3

4

5

6

7

Month

1901-01-01 266.0

1901-02-01 145.9

1901-03-01 183.1

1901-04-01 119.3

1901-05-01 180.3

Name: Sales, dtype: float64

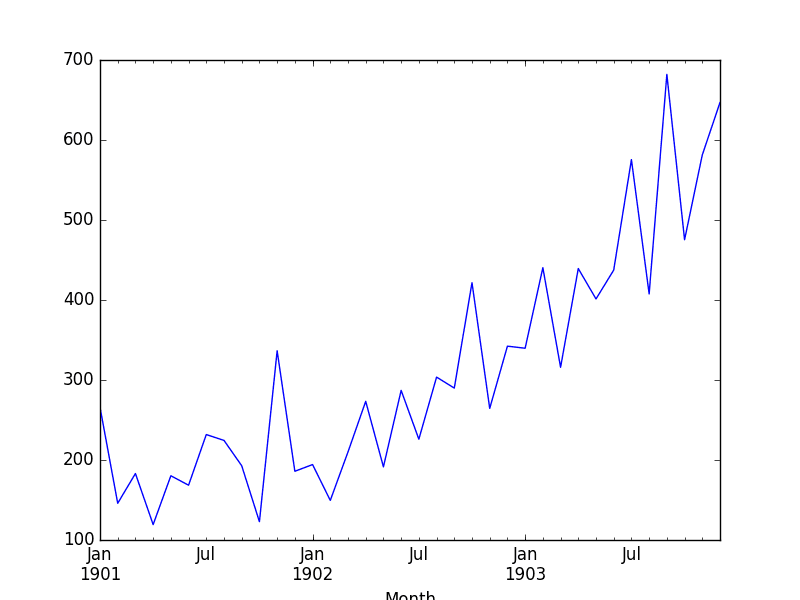

Shampoo Sales Dataset Plot

The data is also plotted as a time series with the month along the x-axis and sales figures on the y-axis.

We can see that the Shampoo Sales dataset has a clear trend. This suggests that the time series is not stationary and will require differencing to make it stationary, at least a difference order of 1.

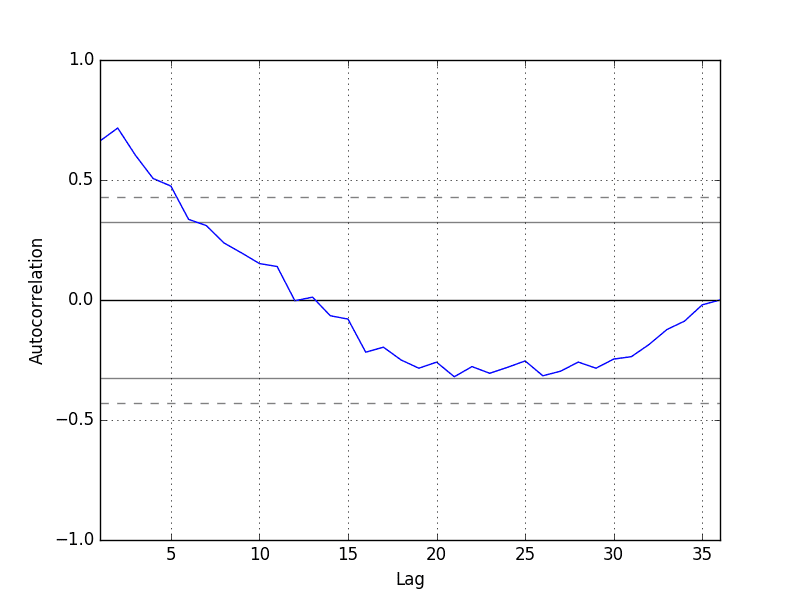

Pandas offers a built-in capability to plot autocorrelations. The following example showcases the autocorrelation for an extensive set of time series lags:

Running the example prints a summary of the fit model. This summarizes the coefficient values used as well as the skill of the fit on the on the in-sample observations.

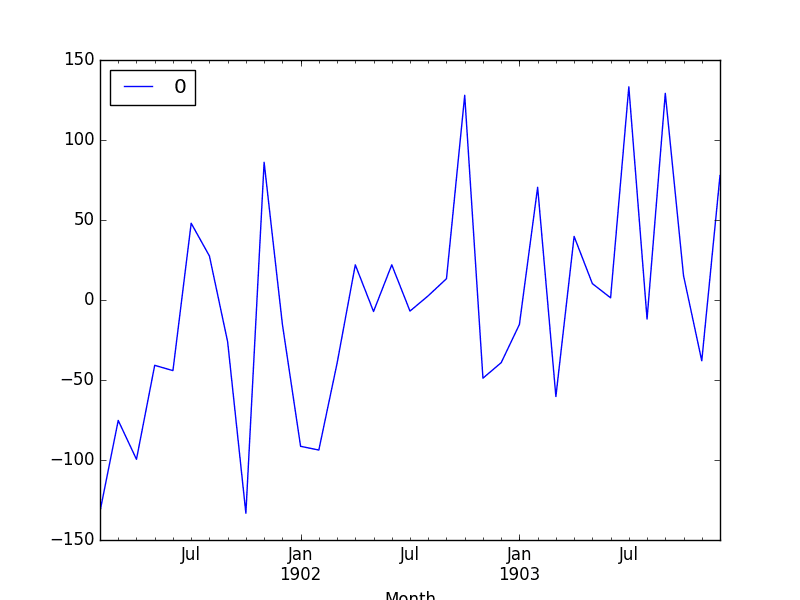

First, we get a line plot of the residual errors, suggesting that there may still be some trend information not captured by the model.

ARMA Fit Residual Error Line Plot

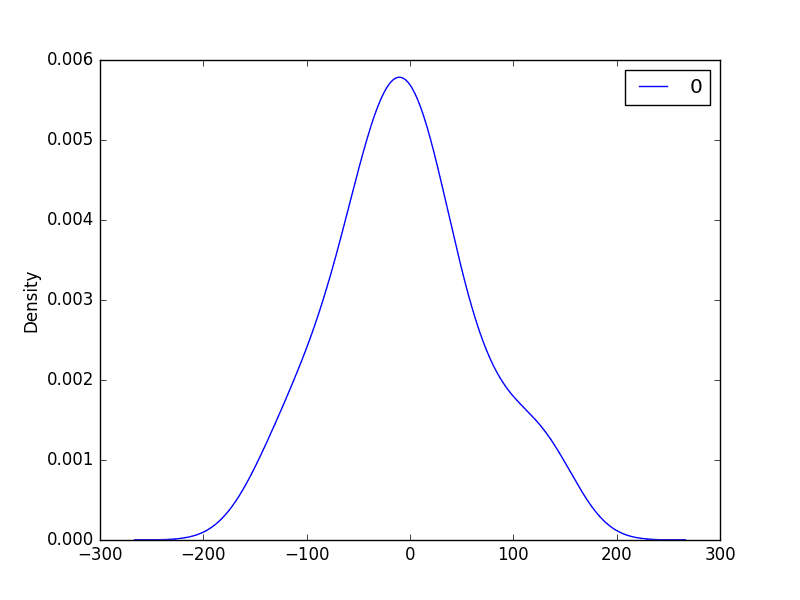

Next, we get a density plot of the residual error values, suggesting the errors are Gaussian, but may not be centred on zero.

ARMA Fit Residual Error Density Plot

The distribution of the residual errors is displayed. The results show that indeed there is a bias in the prediction (a non-zero mean in the residuals).

1

2

3

4

5

6

7

8

count 36.000000

mean 21.936144

std 80.774430

min -122.292030

25% -35.040859

50% 13.147219

75% 68.848286

max 266.000000

Note, that although we used the entire dataset for time series analysis, ideally we would perform this analysis on just the training dataset when developing a predictive model.

Next, let’s look at how we can use the ARIMA model to make forecasts.

Rolling Forecast ARIMA Model

The ARIMA model can be used to forecast future time steps.

The ARIMA model is adept at forecasting future time points. In a rolling forecast, the model is often retrained as new data becomes available, allowing for more accurate and adaptive predictions.

We can use the predict() function on the ARIMAResults object to make predictions. It accepts the index of the time steps to make predictions as arguments. These indexes are relative to the start of the training dataset used to make predictions.

How to Forecast with ARIMA:

Use the predict() function on the ARIMAResults object. This function requires the index of the time steps for which predictions are needed.

To revert any differencing and return predictions in the original scale, set the typ argument to ‘levels’.

For a simpler one-step forecast, employ the forecast() function.

We can split the training dataset into train and test sets, use the train set to fit the model and generate a prediction for each element on the test set.

A rolling forecast is required given the dependence on observations in prior time steps for differencing and the AR model. A crude way to perform this rolling forecast is to re-create the ARIMA model after each new observation is received.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

# evaluate an ARIMA model using a walk-forward validation

We manually keep track of all observations in a list called history that is seeded with the training data and to which new observations are appended each iteration.

Putting this all together, below is an example of a rolling forecast with the ARIMA model in Python.

Running the example prints the prediction and expected value each iteration.

We can also calculate a final root mean squared error score (RMSE) for the predictions, providing a point of comparison for other ARIMA configurations.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

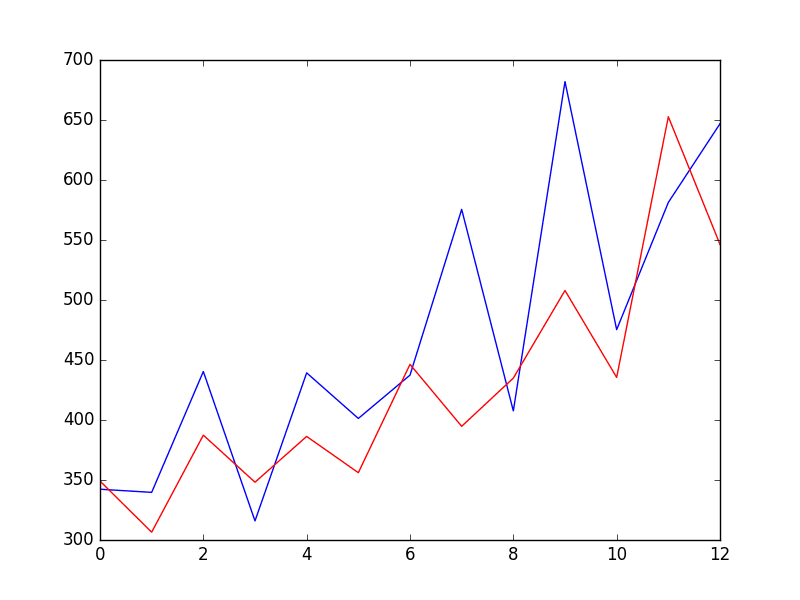

predicted=343.272180, expected=342.300000

predicted=293.329674, expected=339.700000

predicted=368.668956, expected=440.400000

predicted=335.044741, expected=315.900000

predicted=363.220221, expected=439.300000

predicted=357.645324, expected=401.300000

predicted=443.047835, expected=437.400000

predicted=378.365674, expected=575.500000

predicted=459.415021, expected=407.600000

predicted=526.890876, expected=682.000000

predicted=457.231275, expected=475.300000

predicted=672.914944, expected=581.300000

predicted=531.541449, expected=646.900000

Test RMSE: 89.021

A line plot is created showing the expected values (blue) compared to the rolling forecast predictions (red). We can see the values show some trend and are in the correct scale.

ARIMA Rolling Forecast Line Plot

The model could use further tuning of the p, d, and maybe even the q parameters.

Configuring an ARIMA Model

ARIMA is often configured using the classical Box-Jenkins Methodology. This process employs a meticulous blend of time series analysis and diagnostics to pinpoint the most fitting parameters for the ARIMA model.

The Box-Jenkins Methodology: A Three-Step Process:

Model Identification: Begin with visual tools like plots and leverage summary statistics. These aids help recognize trends, seasonality, and autoregressive elements. The goal here is to gauge the extent of differencing required and to determine the optimal lag size.

Parameter Estimation: This step involves a fitting procedure tailored to derive the coefficients integral to the regression model.

Model Checking: Armed with plots and statistical tests delve into the residual errors. This analysis illuminates the temporal structure that the model might have missed.

The process is repeated until either a desirable level of fit is achieved on the in-sample or out-of-sample observations (e.g. training or test datasets).

The process was described in the classic 1970 textbook on the topic titled Time Series Analysis: Forecasting and Control by George Box and Gwilym Jenkins. An updated 5th edition is now available if you are interested in going deeper into this type of model and methodology.

Given that the model can be fit efficiently on modest-sized time series datasets, grid searching parameters of the model can be a valuable approach.

For an example of how to grid search the hyperparameters of the ARIMA model, see the tutorial:

Hi Jason! Great tutorial.

Just a reeal quick question ..how can I fit and run the last code for multiple varialbles?..the dataset that looks like this:

Nice article, it helped me a lot.

I have a question as to how to make predictions in a scenario where you are attempting to make new predictions not included in the dataset.

For each item in the test set, after a prediction is made, the correct data point, taken from test, is added to the history.

How can I make predictions when I don’t have a test set to extract the right data points from?

have a question am doing a project concerning data analytics insights for retail company sales case study certain supermarket in my area and am proposing to use ARIMA can it be appropriate and how can i apply it

I have a usecase of timeseries forecasting where I have to predict sales of different products out of the electronics store. There are around 300 types of different products. And I have to predict the sales on the next day for each of the product based on previous one year data. But not every product is being sold each day.

My guess is I have to create a tsa for each product. but the data quality for each product is low as not each product is being sold each day. And my use case is that I have to predict sales of each product.

Any way I can use time series on whole data without using tsa on each product individually?

Hi I am trying to understand data set related to daily return of a stock. I calculated autocorrelation and partial autocorrelation function as a function of lag. I am observing

that ACF lies within two standard error limits. But I find PACF to be large value at few non-zero lags, one and two. I want to ask you is this behaviour strange ? ACF zero and PACF large and non-zero. If this behaviour not strange, then how does one arrive at the correct order of ARIMA model for this data.

hi. great tutorial.

what’s your advice for finding correlation between two data sets.

I have two csv file, one showing amount of money spent on advertising and one showing amount of sale. and I wanna find out effect of advertisement on sale and forecasting future sale with different amount of advertisement. I know one way is finding correlation with panda like:

sales_df[‘colx’].corr(spend_df[‘coly’])

but I wanna know is there a better way?

For some reason, I need to calculate residuals of a fitted ARMA-GARCH model manually, but found that the calculated residuals are different of those directly from the R package such rugarh. I put the estimated parameters back to the model and use the training data to back out the residuals. How to get the staring residuals at t=0, t=-1 etc. Should I treat the fitted ARMA-GARCH just as an fitted ARMA model? In that case why we need to fit an ARMA-GARCH model to the training data.

Hi Jason,

Could you do a GaussianProcess example with the same data. And compare the two- those two methods seem to be applicable to similar problems- I would love to see your insights.

Thanks. If you also did a comparative study of the two, that would be great- I realize that might be out of the regular, thought I’d still ask. Also can I sign up for email notification?

Hi, appreciate your great explanations, awesome! I wonder how will you load a statistics feature-engineered time series dataset/dataframe into ARIMA? Would appreciate if you have example or article. Thanks!

Hello,

I have climate change data for the past 8 years and I need to do a regression model using climate as a factor so I need at least climate data for 30 years which I can’t find online. Is it possible to get the previous 22 years climate change using ARIMA based on the last 8 years data.

Thank you

I am also working on a similar dataset which is univariate with a timestamp and a categorical value (around 150 distinct categories). Can we use an ARIMA model for this task?

What if there are multiple columns in dataset. For example: Instead of only 1 items like the shampoo, there could be a column with item numbers ranging from 1 – 20 and a column with number of stores and finally a column with respective sales?

OMG. Searching for weeks, never found an article like this one. Thank a lot.

I need your advice please,

I need to predict Retail sales data with variables like weather, sales Discount’, holiday etc.

Which is the best model is to use? And why?

How can decide the best fit model?

(Can I use SARIMAX for this?)

Hi Jason,

Recently I am working on time series prediction, but my research is a little bit complicated for me to understand how to fix a time series models to predict future values of multi targets.

Recently I read your post in multi-step and multivariate time series prediction with LSTM. But my problem have a series input values for every time (for each second we have recorded more than 500 samples). We have 22 inputs and 3 targets. All the data has been collected during 600 seconds and then predict 3 targets for 600 next seconds. Please help me how can solve this problem?

It is noticed we have trend and seasonality pulses for targets during the time.

Traceback (most recent call last):

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 2276, in converter

date_parser(*date_cols), errors=’ignore’)

File “/Users/kevinoost/PycharmProjects/ARIMA/main.py”, line 6, in parser

return datetime.strptime(‘190’+x, ‘%Y-%m’)

TypeError: strptime() argument 1 must be str, not numpy.ndarray

During handling of the above exception, another exception occurred:

Traceback (most recent call last):

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 2285, in converter

dayfirst=dayfirst),

File “pandas/src/inference.pyx”, line 841, in pandas.lib.try_parse_dates (pandas/lib.c:57884)

File “pandas/src/inference.pyx”, line 838, in pandas.lib.try_parse_dates (pandas/lib.c:57802)

File “/Users/kevinoost/PycharmProjects/ARIMA/main.py”, line 6, in parser

return datetime.strptime(‘190’+x, ‘%Y-%m’)

File “/Users/kevinoost/anaconda/lib/python3.5/_strptime.py”, line 510, in _strptime_datetime

tt, fraction = _strptime(data_string, format)

File “/Users/kevinoost/anaconda/lib/python3.5/_strptime.py”, line 343, in _strptime

(data_string, format))

ValueError: time data ‘190Sales of shampoo over a three year period’ does not match format ‘%Y-%m’

During handling of the above exception, another exception occurred:

Traceback (most recent call last):

File “/Users/kevinoost/PycharmProjects/ARIMA/main.py”, line 8, in

series = read_csv(‘shampoo-sales.csv’, header=0, parse_dates=[0], index_col=0, squeeze=True, date_parser=parser)

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 562, in parser_f

return _read(filepath_or_buffer, kwds)

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 325, in _read

return parser.read()

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 815, in read

ret = self._engine.read(nrows)

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 1387, in read

index, names = self._make_index(data, alldata, names)

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 1030, in _make_index

index = self._agg_index(index)

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 1111, in _agg_index

arr = self._date_conv(arr)

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/parsers.py”, line 2288, in converter

return generic_parser(date_parser, *date_cols)

File “/Users/kevinoost/anaconda/lib/python3.5/site-packages/pandas/io/date_converters.py”, line 38, in generic_parser

results[i] = parse_func(*args)

File “/Users/kevinoost/PycharmProjects/ARIMA/main.py”, line 6, in parser

return datetime.strptime(‘190’+x, ‘%Y-%m’)

File “/Users/kevinoost/anaconda/lib/python3.5/_strptime.py”, line 510, in _strptime_datetime

tt, fraction = _strptime(data_string, format)

File “/Users/kevinoost/anaconda/lib/python3.5/_strptime.py”, line 343, in _strptime

(data_string, format))

ValueError: time data ‘190Sales of shampoo over a three year period’ does not match format ‘%Y-%m’

Hi Kevin,

the last line of the data set, at least in the current version that you can download, is the text line “Sales of shampoo over a three year period”. The parser barfs on this because it is not in the specified format for the data lines. Try using the “nrows” parameter in read_csv.

series = read_csv(‘~/Downloads/shampoo-sales.csv’, header=0, nrows=36, parse_dates=[0], index_col=0, squeeze=True, date_parser=parser)

Let say I have a time series data with many attribute. For example a row will have (speed, fuel, tire_pressure), how could we made a model out of this ? the value of each column may affect each other, so we cannot do forecasting on solely 1 column. I google a lot but all the example I’ve found so far only work on time series of 1 attribute.

Update: the statsmodels.tsa.arima_model.ARIMA() function documentation says it takes the optional parameter exog, which is described in the documentation as ‘an optional array of exogenous variables’. This sounds like multivariate analysis to me, would you agree?

I am trying to predict number of cases of a mosquito-borne disease, over time, given weather data. So I believe the ARIMA model should work for this, correct?

Hi, would you have a example for the seasonal ARIMA post? I have installed latest statsmodels module, but there is an error of import the SARIMAX. Do help if you manage to figure it out. Thanks.

– Just to be sure. model_fit.forecast() is single step ahead forecasts and model_fit.predict() is for multiple step ahead forecasts?

– I am working with a series that seems at least quite similar to the shampoo series (by inspection). When I use predict on the training data, I get this zig-zag pattern in the prediction as well. But for the test data, the prediction is much smoother and seems to saturate at some level. Would you expect this? If not, what could be wrong?

Concerning the second question. Yes, you are right the prediction is not very accurate. But moreover, the predicted time series has a totally different frequency content. As I said, it is smooth and not zig-zaggy as the original data. Is this normal or am I doing something wrong. I also tried the multiple step prediction (model_fit.predict()) on the training data and then the forecast seem to have more or less the same frequency content (more zig-zaggy) as the data I am trying to predict.

In the case of predicting on the training dataset, the model has access to real observations. For example, if you predict the next 5 obs somewhere in the training dataset, it will use obs(t+4) to predict t+5 rather than prediction(t+4).

In the case of predicting beyond the end of the model data, it does not have obs to make predictions (unless you provide them), it only has access to the predictions it made for prior time steps. The result is the errors compound and things go off the rails fast (flat forecast).

Continuing on this note, how far ahead can you forecast using something like ARIMA or AR or GARCH in Python? I’m guessing most of these utilize some sort of Kalman filter forecasting mechanism?

To give you a sense of my data, given between 60k and 80k data points, how far ahead in terms of number of predictions can we make reliably? Similar to Sebastian, I have pretty jagged predictions in-sample, but essentially as soon as the valid/test area begins, I have no semblance of that behavior and instead just get a pretty flat curve. Let me know what you think. Thanks!

The skill of AR+GARH (or either) really depends on the choice of model parameters and on the specifics of the problem.

Perhaps you can try grid searching different parameters?

Perhaps you can review ACF/PACF plots for your data that may suggest better parameters?

Perhaps you can try non-linear methods?

Perhaps your problem is truly challenging/not predictable?

In step 3, when it says “Prediction: 46.755211”, is that meaning after it fit the model on the dataset, it uses the model to predict what would happen next from the dataset, right?

thank you very much for the post, very good written! I have a question: so I used your approach to build the model, but when I try to forecast the data that are out of sample, I commented out the obs = test[t] and change history.append(obs) to history.append(yhat), and I got a flat prediction… so what could be the reason? and how do you actually do the out-of-sample predictions based on the model fitted on train dataset? Thank you very much!

Each loop in the rolling forecast shows you how to make a one-step out of sample forecast.

Train your ARIMA on all available data and call forecast().

If you want to perform a multi-step forecast, indeed, you will need to treat prior forecasts as “observations” and use them for subsequent forecasts. You can do this automatically using the predict() function. Depending on the problem, this approach is often not skillful (e.g. a flat forecast).

Hello Jason, thanks for this amazing post.

I was wondering how does the “size” work here. For example lets say i want to forecast only 30 days ahead. I keep getting problems with the degrees of freedom.

Could you please explain this to me.

Thank you for explaining the ARIMA model in such clear detail.

It helped me to make my own model to get numerical forrcasts and store it in a database.

So nice that we live in an era where knowledge is de-mystified .

Hi Jason,

Lucky i found this at the begining of my project.. Its a great start point and enriching.

Keep it coming :).

This can also be used for non linear time series as well?

Hi Jason,

Great writeup, had a query, when u have a seasonal data and do seasonal differencing. i.e for exy(t)=y(t)-y(t-12) for yearly data. What will be the value of d in ARIMA(p,d,q).

ARIMA will not do seasonal differencing (there is a version that will called SARIMA). The d value on ARIMA will be unrelated to the seasonal differencing and will assume the input data is already seasonally adjusted.

Thanks for the great post! It was very helpful. I’m currently trying to forecast with the ARIMA model using order (4, 1, 5) and I’m getting an error message “The computed initial MA coefficients are not invertible. You should induce invertibility, choose a different model order, or you can pass your own start_params.” The model works when fitting, but seems to error out when I move to model_fit = model.fit(disp=0). The forecast works well when using your parameters of (0, 1, 5) and I used ACF and PACF plots to find my initial p and q parameters. Any ideas on the cause/fix for the error? Any tips would be much appreciated.

Sorry, it is difficult for (3,1,3) as well.

It worked for prediction for the first step of the test data, but gave out the error on the second prediction step.

Good afternoon!

Is there an analog to the function auto.arima in the package for python from the package of the language R.

For automatic selection of ARIMA parameters?

Thank you!

Hi. Great one. Suppose I have multiple airlines data number of passengers for two years recorded on daily basis. Now I want to predict for each airline number of possible passangers on next few months. How can I fit these time series models. Separate model for each airline or one single model?

Hi Jason, if in my dataset, my first column is date (YYYYMMDD) and second column is time (hhmmss) and third column is value at given date and time. So could I use ARIMA model for forecasting such type of time series ?

Hi Jason,

I have a general question about ARIMA model in the case of multiple Time Series:

suppose you have not only one time series but many (i.e. the power generated per hour at 1000 different wind farms). So you have a dataset of 1000 time series of N points each and you want to predict the next N+M points for each of the time series.

Analyzing each time series separately with the ARIMA could be a waste. Maybe there are similarities in the time evolution of these 1000 different patterns which could help my predictions. What approach would you suggest in this case?

Hi Jason and thank you for this post, its really helpful!

I have one question regarding ARIMA computation time.

I’m working on a dataset of 10K samples, and I’ve tried rolling and “non rolling” (where coefficients are only estimated once or at least not every new sample) forecasting with ARIMA :

– rolling forecast produces good results but takes a big amount of time (I’m working with an old computer, around 3/6h depending on the ARMA model);

– “non rolling” doesn’t forecast well at all.

Re-estimating the coefficients for each new sample is the only possibility for proper ARIMA forecasting?

Dear Respected Sir, I have tried to use ARIMA model for my dataset, some samples of my dataset are following,

YYYYMMDD hhmmss Duration

20100916 130748 18

20100916 131131 99

20100916 131324 214

20100916 131735 72

20100916 135342 37

20100916 144059 250

20100916 150148 87

20100916 150339 0

20100916 150401 180

20100916 154652 248

20100916 183403 0

20100916 210148 0

20100917 71222 179

20100917 73320 0

20100917 81718 25

20100917 93715 15

But when I used ARIMA model for such type of dataset, the prediction was very bad and test MSE was very high as well, My dataset has irregular pattern and autocorrelation is also very low. so could ARIMA model be used for such type of dataset ? or I have to do some modification in my dataset for using ARIMA model?

Looking forward.

Thanks

Love this. The code is very straightforward and the explanations are nice.

I would like to see a HMM model on here. I have been struggling with a few different packages (pomegranate and hmmlearn) for some time now. would like to see what you can do with it! (particularly a stock market example)

Good evening,

In what I am doing, I have a training set and a test set. In the training set, I am fitting an ARIMA model, let’s say ARIMA(0,1,1) to the training set. What I want to do is use this model and apply it to the test set to get the residuals.

So far I have:

model = ARIMA(data,order = (0,1,1))

model_fit = model.fit(disp=0)

res = model_fit.resid

This gives me the residuals for the training set. So I want to apply the ARIMA model in ‘model’ to the test data.

Is there a function to do this?

Thank you

You could use your fit model to make a prediction for the test dataset then compare the predictions vs the real values to calculate the residual errors.

In your example, you append the real data set to the history list- aren’t you supposed to append the prediction?

history.append(obs), where obs is test[t].

in a real example, you don’t have access to the real “future” data. if you were to continue your example with dates beyond the data given in the csv, the results are poor. Can you elaborate?

interestingly, under your Rolling Forecast ARIMA Model explanation, matplotlib was above statsmodels.

from matplotlib import pyplot

from statsmodels.tsa.arima_model import ARIMA

i am using jupyter notebook from WinPython-64bit-3.5.3.1Qt5 to run your examples. i keep getting ImportError: No module named ‘statsmodels’ if i declare import this way in ARIMA with Python explanation

from matplotlib import pyplot

from pandas import DataFrame

from statsmodels.tsa.arima_model import ARIMA

i think it could be i need to restart the virtual environment to let the environment recognize it, today i re-test the following declarations it is ok.

from matplotlib import pyplot

from pandas import DataFrame

from statsmodels.tsa.arima_model import ARIMA

Great explanation

can anyone help me to write code in R about forecasting such as (50,52,50,55,57) i need to forecasting the next 3 hour, kindly help me to write code using R with ARIMA and SARIMA Model

thanks in advance

Can the ACF be shown using bars so you can look to see where it drops off when estimating order of MA model? Or have you done a tutorial on interpreting ACF/PACF plots please elsewhere?

I am getting the error when trying to run the code:

from matplotlib import pyplot

from pandas import DataFrame

from pandas.core import datetools

from pandas import read_csv

from statsmodels.tsa.arima_model import ARIMA

series = read_csv(‘sales-of-shampoo-over-a-three-year.csv’, header=0, parse_dates=[0], index_col=0)

# fit model

model = ARIMA(series, order=(0, 0, 0))

model_fit = model.fit(disp=0)

print(model_fit.summary())

# plot residual errors

residuals = DataFrame(model_fit.resid)

residuals.plot()

pyplot.show()

residuals.plot(kind=’kde’)

pyplot.show()

print(residuals.describe())

Error Mesg on Console :

C:\Python36\python.exe C:/Users/aamrit/Desktop/untitled1/am.py

C:/Users/aamrit/Desktop/untitled1/am.py:3: FutureWarning: The pandas.core.datetools module is deprecated and will be removed in a future version. Please use the pandas.tseries module instead.

from pandas.core import datetools

Traceback (most recent call last):

File “C:\Python36\lib\site-packages\pandas\core\tools\datetimes.py”, line 444, in _convert_listlike

values, tz = tslib.datetime_to_datetime64(arg)

File “pandas\_libs\tslib.pyx”, line 1810, in pandas._libs.tslib.datetime_to_datetime64 (pandas\_libs\tslib.c:33275)

TypeError: Unrecognized value type:

During handling of the above exception, another exception occurred:

Traceback (most recent call last):

File “C:\Python36\lib\site-packages\statsmodels\tsa\base\tsa_model.py”, line 56, in _init_dates

dates = to_datetime(dates)

File “C:\Python36\lib\site-packages\pandas\core\tools\datetimes.py”, line 514, in to_datetime

result = _convert_listlike(arg, box, format, name=arg.name)

File “C:\Python36\lib\site-packages\pandas\core\tools\datetimes.py”, line 447, in _convert_listlike

raise e

File “C:\Python36\lib\site-packages\pandas\core\tools\datetimes.py”, line 435, in _convert_listlike

require_iso8601=require_iso8601

File “pandas\_libs\tslib.pyx”, line 2355, in pandas._libs.tslib.array_to_datetime (pandas\_libs\tslib.c:46617)

File “pandas\_libs\tslib.pyx”, line 2538, in pandas._libs.tslib.array_to_datetime (pandas\_libs\tslib.c:45511)

File “pandas\_libs\tslib.pyx”, line 2506, in pandas._libs.tslib.array_to_datetime (pandas\_libs\tslib.c:44978)

File “pandas\_libs\tslib.pyx”, line 2500, in pandas._libs.tslib.array_to_datetime (pandas\_libs\tslib.c:44859)

File “pandas\_libs\tslib.pyx”, line 1517, in pandas._libs.tslib.convert_to_tsobject (pandas\_libs\tslib.c:28598)

File “pandas\_libs\tslib.pyx”, line 1774, in pandas._libs.tslib._check_dts_bounds (pandas\_libs\tslib.c:32752)

pandas._libs.tslib.OutOfBoundsDatetime: Out of bounds nanosecond timestamp: 1-01-01 00:00:00

During handling of the above exception, another exception occurred:

Traceback (most recent call last):

File “C:/Users/aamrit/Desktop/untitled1/am.py”, line 9, in

model = ARIMA(series, order=(0, 0, 0))

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 997, in __new__

return ARMA(endog, (p, q), exog, dates, freq, missing)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 452, in __init__

super(ARMA, self).__init__(endog, exog, dates, freq, missing=missing)

File “C:\Python36\lib\site-packages\statsmodels\tsa\base\tsa_model.py”, line 44, in __init__

self._init_dates(dates, freq)

File “C:\Python36\lib\site-packages\statsmodels\tsa\base\tsa_model.py”, line 58, in _init_dates

raise ValueError(“Given a pandas object and the index does ”

ValueError: Given a pandas object and the index does not contain dates

Traceback (most recent call last):

File “C:/Users/aamrit/Desktop/untitled1/am.py”, line 10, in

model_fit = model.fit(disp=0)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 1151, in fit

callback, start_ar_lags, **kwargs)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 956, in fit

start_ar_lags)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 578, in _fit_start_params

start_params = self._fit_start_params_hr(order, start_ar_lags)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 508, in _fit_start_params_hr

endog -= np.dot(exog, ols_params).squeeze()

TypeError: Cannot cast ufunc subtract output from dtype(‘float64’) to dtype(‘int64’) with casting rule ‘same_kind’

Code :

import pandas as pd

import numpy as np

import matplotlib.pylab as plt

from datetime import datetime

from statsmodels.tsa.arima_model import ARIMA

data = pd.read_csv(‘AirPassengers.csv’, header=0, parse_dates=[0], index_col=0)

model = ARIMA(data, order=(1,1,0),exog=None, dates=None, freq=None, missing=’none’)

model_fit = model.fit(disp=0)

print(model_fit.summary())

@kyci is correct as you can check in https://github.com/statsmodels/statsmodels/issues/3504.

I was following this tutorial for my dataset, and what fixed my problem was just converting to float, like this:

X = series.values

X = X.astype(‘float32’)

Traceback (most recent call last):

File “C:/untitled1/prediction_new.py”, line 31, in

output = model_fit.predict(start=’2017-01-08′,end=’2017-20-08′)

File “C:\Python36\lib\site-packages\statsmodels\base\wrapper.py”, line 95, in wrapper

obj = data.wrap_output(func(results, *args, **kwargs), how)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 1492, in predict

return self.model.predict(self.params, start, end, exog, dynamic)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 733, in predict

start = self._get_predict_start(start, dynamic)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 668, in _get_predict_start

method)

File “C:\Python36\lib\site-packages\statsmodels\tsa\arima_model.py”, line 375, in _validate

start = _index_date(start, dates)

File “C:\Python36\lib\site-packages\statsmodels\tsa\base\datetools.py”, line 52, in _index_date

date = dates.get_loc(date)

AttributeError: ‘NoneType’ object has no attribute ‘get_loc’

ERROR is

runfile(‘C:/Users/kashi/Desktop/prog/Date_time.py’, wdir=’C:/Users/kashi/Desktop/prog’)

Traceback (most recent call last):

File “”, line 1, in

runfile(‘C:/Users/kashi/Desktop/prog/Date_time.py’, wdir=’C:/Users/kashi/Desktop/prog’)

File “C:\Users\kashi\Anaconda3\lib\site-packages\spyder\utils\site\sitecustomize.py”, line 866, in runfile

execfile(filename, namespace)

File “C:\Users\kashi\Anaconda3\lib\site-packages\spyder\utils\site\sitecustomize.py”, line 102, in execfile

exec(compile(f.read(), filename, ‘exec’), namespace)

File “C:/Users/kashi/Desktop/prog/Date_time.py”, line 10, in

series = read_csv(‘E:/data/csv/shampoo-sales.csv’, header=0, parse_dates=[0], index_col=0, squeeze=True, date_parser=parser)

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\parsers.py”, line 562, in parser_f

return _read(filepath_or_buffer, kwds)

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\parsers.py”, line 325, in _read

return parser.read()

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\parsers.py”, line 815, in read

ret = self._engine.read(nrows)

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\parsers.py”, line 1387, in read

index, names = self._make_index(data, alldata, names)

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\parsers.py”, line 1030, in _make_index

index = self._agg_index(index)

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\parsers.py”, line 1111, in _agg_index

arr = self._date_conv(arr)

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\parsers.py”, line 2288, in converter

return generic_parser(date_parser, *date_cols)

File “C:\Users\kashi\Anaconda3\lib\site-packages\pandas\io\date_converters.py”, line 38, in generic_parser

results[i] = parse_func(*args)

File “C:/Users/kashi/Desktop/prog/Date_time.py”, line 8, in parser

return datetime.strptime(‘190’+x, ‘%Y-%m’)

File “C:\Users\kashi\Anaconda3\lib\_strptime.py”, line 510, in _strptime_datetime

tt, fraction = _strptime(data_string, format)

File “C:\Users\kashi\Anaconda3\lib\_strptime.py”, line 343, in _strptime

(data_string, format))

ValueError: time data ‘1901-Jan’ does not match format ‘%Y-%m’

I have already removed the footer note from the dataset and I also open dataset in text editor. But I couldn’t remove this error. But when I comment ”date_parser=parser” my code runs but doesn’t show years,

How to resolve it?

Thanks

File “/shampoo.py”, line 6, in parser

return datetime.strptime(‘190’+x, ‘%Y-%m’)

TypeError: ufunc ‘add’ did not contain a loop with signature matching types dtype(‘<U32') dtype('<U32') dtype('<U32')

I've tried '%Y-%b' but that only gives me the "does not match format" error.

Hey,

I’ve two years monthly data of different products and their sales at different stores. How can I perform Time series forecasting on each product at each location?

You mentioned that since the residuals doesn’t have mean = 0, there is a bias. I have same situation. But the spread of the residuals is in the order of 10^5. So i thought it is okay to have non-zero mean. Your thoughts please?

Firstly, I would like to thanks about your sharing

Secondly, I have a small question about ARIMA with Python. I have about 700 variables need to be forecasted with ARIMA model. How Python supports this issuse Jason

For example, I have data of total orders in a country, and it will be contributte to each districts

So I need to forecast for each districts (about 700 districts)

The result of model_fit.forecast() is like (array([ 242.03176448]), array([ 91.37721802]), array([[ 62.93570815, 421.12782081]])). The first number is yhat, can you explain what the other number means in the result? thank you!

Great blogpost Jason!

Had a follow up question on the same topic.

Is it possible to do the forecast with the ARIMA model at a higher frequency than the training dataset?

For instance, let’s say the training dataset is sampled at 15min interval and after building the model, can I forecast at 1second level intervals?

If not directly as is, any ideas on what approaches can be taken? One approach I am entertaining is creating a Kernel Density Estimator and sampling it to create higher frequency samples on top of the forecasts.

Thanks, much appreciate your help!

Hmm, it might not be the best tool. You might need something like a neural net so that you can design a one-to-many mapping function for data points over time.

Your tutorial was really helpful to understand the concept of solving time series forecasting problem. But I have small doubt regarding the steps you followed at the very end. I’m pasting your code down below-

X = series.values

size = int(len(X) * 0.66)

train, test = X[0:size], X[size:len(X)]

history = [x for x in train]

predictions = list()

for t in range(len(test)):

model = ARIMA(history, order=(5,1,0))

model_fit = model.fit(disp=0)

output = model_fit.forecast()

yhat = output[0]

predictions.append(yhat)

obs = test[t]

history.append(obs)

print(‘predicted=%f, expected=%f’ % (yhat, obs))

error = mean_squared_error(test, predictions)

Note:1) here in the above for each iteration you’re adding the elements from the “test” and the forecasted value because in real forecasting we don’t have future data to include in test, isn’t it? Or is it that your’re trying to explain something and I’m not getting it.

2) Second doubt, aren’t you suppose to perform “reverse difference” for that you have used first order differencing in the model?

Kindly, please clear my doubt

Note: I have also went through one of your other tutorial where you have forecasted the average daily temperature in Australia.

here the steps you followed were convincing, also you have performed “inverse difference” step to scale the prediction to original scale.

I have followed the steps from the one above but I m unable to forecast correctly.

Hi Jason,

Recently I am working on time series prediction, but my research is a little bit complicated for me to understand how to fix a time series models to predict future values of multi targets.

Recently I read your post in multi-step and multivariate time series prediction with LSTM. But my problem have a series input values for every time (for each second we have recorded more than 500 samples). We have 22 inputs and 3 targets. All the data has been collected during 600 seconds and then predict 3 targets for 600 next seconds. Please help me how can solve this problem?

It is noticed we have trend and seasonality pulses for targets during the time.

Hey just a quick check with you regarding the prediction part. I need to do some forecast of future profit based on the data from past profit. Let’s say I got the data for the past 3 years, and then I wanted to perform a forecast on the next 12 months in next year. Does the model above applicable in this case?

Hey Jason thanks so much for the clarification! But just to clarify, when I run the example above, my inputs are the past records for the past 3 years grouped by month. Then, how the code actually plot out the forecasted graph is basically takes in those input and plot, am I right? So, can I assumed that the graph that plotted out is meant for the prediction of next year?

Hey Jason, thanks so much for the replies! But just to check with you, which line of the code should I modify so that it will only predict for the next 12 months instead of 13?

Also, just to be sure, if I were to predict for the profit for next year, the value that I should take should be the predicted rather than expected, am I right?

Hey Jason, thanks so much but I am still confused as I am new to data analytic. The model above aims to make a prediction on what you already have or trying to forecast on what you do not have?

Also, may I check with you on how it works? Because I downloaded the sample dataset and the dataset contains the values of past 3 years grouped by months. So, can I assume the prediction takes all the values from past years into account in order to calculate for the prediction value? Or it simply takes the most recent one and calculate for the prediction?

Hey Jason, I am so sorry for the spams. But just a quick check with you again, let’s say I have some zero value for the profit, will it break the forecast function? Or the forecast function must take in all non-zero value. Because sometimes I am getting “numpy.linalg.linalg.LinAlgError: SVD did not converge” error message and I not sure if it is the zero values that is causing the problem. 🙂

Hi Jason, thanks so much for the share! The tutorial was good! However, when I am using my own data set, I am getting the same error message as one of the guy above. The error message is ‘numpy.linalg.linalg.LinAlgError: SVD did not converge’.

I tried to crack my head out trying to observe the data sets that caused the error message but I could not figure out anything. I tried with 0 value and very very very drastic drop or increase in the data, some seems okay but at some point, some data set will just fail and return the error message.

May I know what kind of data or condition will trigger the error above so I can take extra precaution when preparing the data?

I tried with multiple set of data without a single zero. I realized a problem but I not sure if my observation is correct as I am still trying to figure out how the code above works, for that part I might need your enlightenment.

Let’s say the data is 1000, 100, 10000 respectively to first, second and third year. This kind of data will throw out the error message above. So can I assume that, as long as there is a big drastic drop/increase in the data set, in this case from 100 to 10000, this kind of condition will execute with error?

Thank you for the tutorial, it’s great! I have a question about stationarity and differencing. If time series is non stationary but is made stationary with simple differencing, are you required to have d=1 in your selected model? Can I choose a Model with no differencing for this data if it gives me a better root mean square error and there is no evidence of autocorrelation?

@Jason, This article has helped me a lot for the training set predictions which i had managed to do earlier too, but could you help me with the future forecasting, let say your date data is till 10th November, 2017 and i want to predict the values for the next one week or next 3 days..

For future predictions, let say i have data till 10th November, and based on your analysis as shown above, can you help me with the future predictions for a week or so, need an idea of how to predict future data..

– We need to ensure that the residuals of our model are uncorrelated and normally distributed with zero mean.

What if the residuals are not normally distributed?

It would be very grateful if you could explain how to approach in such scenario.

@Jason, What if we don’t want Rolling forecast, which means, my forecast should only be based on the training data, and it should predict the test data..

I am using the below code:

X = ts.values

size = int(len(X) * 0.75)

train, test = X[0:size], X[size:len(X)]

model = ARIMA(train, order=(4, 1, 2))

results_AR = model.fit(disp=0)

preds=results_AR.predict(size+1,size+16)

pyplot.plot(test[0:17])

pyplot.plot(preds, color=’red’)

pyplot.show()

This prediction is giving me really bad results, need urgent help on this.

Hi Jason, I have two questions.

1. Let’s say I want to estimate an AR model like this: x(t)=a*x(t-2) + e. If I use ARIMA(2,0,0), it will add the term x(t-1) as well, which I don’t want. In SAS I would use p=(2) on the estimate statement of proc arima rather than p=2.

2. How do I incorporate covariates? For example, a simple model like this: x(t)=a*x(t-2) + b*f(t) + e, where f(t) e.g. is 1 if it’s the month of January and 0 otherwise.

Thanks.

I am getting the following error when loading the series dataframe in python

“ValueError: time data ‘190Sales of shampoo over a three year period’ does not match format ‘%Y-%m'”

Ive just copy pasted the code from this website but its not working. Any suggestions? Im using Sypder

Hello,

Is it possible to predict hourly temperature for upcoming 5 years based on hourly temperature data of last 5 years ?

I am trying this out with ARIMA model, its giving me vrey bad output ( attenuating curve ).

if the time series corresponds to brownian motion time series generated with different Hurst value (let’s say H1 = 0.6 and H2 = 0.7), is this model a good fit to classify if it is H1 or H2?

I have followed all of your posts related to Time Series to do my first data science project. I have done the parameter optimization also. The same code is working in my laptop but when i ran in Kaggle it shows “The computed initial AR coefficients are not stationary

You should induce stationarity, choose a different model order, or you can

pass your own start_params”. The python version is same in my environment and in Kaggle. Is this common?

Also, just to double confirm with you on my understanding, basically what the algorithm does is, take in all input in csv and fit into model, perform a forecast, append the forecast value into the model, then go thru the for loop again to recreate a new ARIMA model, forecast then append new forecast value, then go thru the for loop again?

In addition, the next row prediction is always depends on the past prediction values?

Thanks Jason for making it simple. I run the program but getting error

1st error :

TypeError: Cannot cast ufunc subtract output from dtype(‘float64’) to dtype(‘int64’) with casting rule ‘same_kind’

After changing code , i got 2nd error

model = ARIMA(series.astype(float), order=(5,1,0))

I m getting following error

LinAlgError: SVD did not converge

Looks like the data might have some issues. Perhaps calculate some summary stats, visualizations and look at the raw data to see if there is anything obvious.

Thanks Jason for the quick response. Now i tried for Sampoo dataset, getting following error :

ValueError: time data ‘1901-Jan’ does not match format ‘%d-%m’

When we use a recursive model for ARIMA, let say like saw in one of your examples:

1

2

3

4

5

6

7

8

9

10

11

12

fortinrange(len(test)):

try:

model=ARIMA(history,order=(4,0,2))

model_fit=model.fit(disp=0)

output=model_fit.forecast()

yhat=output[0]

predictions.append(yhat)

obs=test[t]

history.append(obs)

except(ValueError,LinAlgError):

pass

print('predicted=%f, expected=%f'%(yhat,obs))

Why my final test vs predicted graph is coming as if, the predictions are following the test values, it’s like if test is following a pattern, predictions is following similar pattern, hence ultimately our ARIMA predictions isn’t working properly, i hope you got my point.

For example: if test[0] keeps increasing till test[5] and decreases, then prediction[1] keeps increasing till predictions[5] and decreases..

Hello! Thank you for this great tutorial. It’d be a great help if you guide me through one of my problems.

I want to implement a machine learning model to predict(forecast) points scored by each player in the upcoming game week.

Say I have values for a player (Lukaku) for 28 game weeks and I train my model based on some selected features for those 28 weeks. How do I predict the outcome of the 29th week?

I am trying to predict total points to be scored by every player for the coming game week.

So basically what should be the input to my model for 29th game week? Since the game assigns points as per live football games happening during the week, I wont have any input data for 29th week.

I have a question on your Rolling Forecast ARIMA model.

When your are appending obs (test(t)) on each step to history, aren’t we getting data leakage?

The test set is supposed to be unseen data, right? Or are you using the test set as a validation set?

oh I see, i misunderstood this assumption, sorry. But how can I predict multiple steps? I used the predict() method from ARIMA model but the results were weird.

Very nice introduction! Thank you very much for always bringing us excellent ML knowledge.

Can you further explain why you chose (p,d,q) = (5,1,0)? Or you did gird search (which you show in other blogs) using training/test sets to find minimum msg appears at (5,1,0)? Did you know any good reference for diagnostic plots for the hyper-parameters grid searching?

Meanwhile, I am interested in both time-series book and LSTM book. If I purchased both, any further deal?

Thank you for your answer. I have purchased time series book.

I still have few more questions on ARIMA model:

(1) The shampoo sale data obviously shows non-stationary; strictly speaking, we should transform data until it becomes stationary data by taking logarithm and differencing (Box-Cox transformation), and then apply to ARIMA model. Is it correct?

(2) Does the time series data with first-order differencing on ARIMA (p,0,q) give the similar results to the time series data without differencing on ARIMA(p,1,q)? i.e. d = 1 in ARIMA(p,d,q)

equivalently process data with first-order difference?

(3) In this example, we chose ARIMA (5,1,0) and p=5 came from the autocorrelation plot. However, what I read from the book https://www.otexts.org/fpp/8/5 said to judge value of p, we should check PACF plot, instead ACF. Are there any things I missed or misunderstood?

I am also trying to figure out what the other elements of output represent but Jason the link you provided does not work. Could you provide a fresh link?

Thank you for your efforts … i have question

i’m using the following code as mentioned above

def parser(x):

return datetime.strptime(‘190’ +x, ‘%Y-%m’)

but the error appears :

ValueError: time data ‘1902-Jan’ does not match format ‘%Y-%m’

Hey Jason,

Best article I have ever seen. Currently I am working on data driven time series forecasting with PYTHON by ARIMA model. I have data of appliance energy which depends on 26 variables over period of 4 months. My question is how can I use 26 variables to forecast the future value?

Hey Jason, I am new to data analytics. From the chart, may I know how you determined it is stationary or non-stationary as well as how do you see whether it has a lagged value?

Hello! I think you may have made a mistake in the following paragraph.

“If we used 100 observations in the training dataset to fit the model, then the index of the next time step for making a prediction would be specified to the prediction function as start=101, end=101. This would return an array with one element containing the prediction.”

Since python is zero-indexed, the index of the next time step for making a prediction should be 100, I think.

Hi Jason,

great tutorial, as always! Thank you very much for providing your excellent knowledge to the vast community! You really helped me to get a better understanding of this ARIMA type of models.

Do you plan to make a tutorial on nonlinear time-series models such as SETAR? Would be great, because I could not really find anything in this region.

Hi Jason

I tried the code with my data. ACF, PACF plots aren’t showing me any significant correlations. Is there anything by which I can still try the forecast? What should be one’s steps on encounter of such data?

Hello Jason, I have been following your articles and it has been very helpful.

I am running the same code above and get following error:

ValueError Traceback (most recent call last)

in ()

7 pred=list()

8 for i in range(len(test)):

—-> 9 model=ARIMA(history,order=(5,1,0))

10 model_fit=model.fit(disp=0)

11 output=model_fit.forecast()

~\AppData\Local\Continuum\anaconda3\lib\site-packages\statsmodels\tsa\arima_model.py in __new__(cls, endog, order, exog, dates, freq, missing)

998 else:

999 mod = super(ARIMA, cls).__new__(cls)

-> 1000 mod.__init__(endog, order, exog, dates, freq, missing)

1001 return mod

1002

~\AppData\Local\Continuum\anaconda3\lib\site-packages\statsmodels\tsa\arima_model.py in __init__(self, endog, order, exog, dates, freq, missing)

1013 # in the predict method

1014 raise ValueError(“d > 2 is not supported”)

-> 1015 super(ARIMA, self).__init__(endog, (p, q), exog, dates, freq, missing)

1016 self.k_diff = d

1017 self._first_unintegrate = unintegrate_levels(self.endog[:d], d)

~\AppData\Local\Continuum\anaconda3\lib\site-packages\statsmodels\tsa\arima_model.py in __init__(self, endog, order, exog, dates, freq, missing)

452 super(ARMA, self).__init__(endog, exog, dates, freq, missing=missing)

453 exog = self.data.exog # get it after it’s gone through processing

–> 454 _check_estimable(len(self.endog), sum(order))

455 self.k_ar = k_ar = order[0]

456 self.k_ma = k_ma = order[1]

~\AppData\Local\Continuum\anaconda3\lib\site-packages\statsmodels\tsa\arima_model.py in _check_estimable(nobs, n_params)

438 def _check_estimable(nobs, n_params):

439 if nobs 440 raise ValueError(“Insufficient degrees of freedom to estimate”)

441

442

ValueError: Insufficient degrees of freedom to estimate

the code used

from sklearn.metrics import mean_squared_error

size = int(len(df) * 0.66)

train,test=df[0:size],df[size:len(df)]

print(train.shape)

print(test.shape)

history=[x for x in train]

pred=list()

for i in range(len(test)):

model=ARIMA(history,order=(5,1,0))

model_fit=model.fit(disp=0)

output=model_fit.forecast()

yhat=output[0]

pred.append(yhat)

obs=test[i]

history.append(obs)

print(‘predicted = %f,expected = %f’,(yhat,obs))

error=mean_squared_error(test,pred)

print(‘Test MSE: %.3f’ % error)

On;ly change I have made in code is date index. I have done something like this for dates

dt=pd.date_range(“2015-01-01”, “2017-12-1″, freq=”MS”)

Can you explain what is wrong?

also,

I was under impression that you use auto_corr function to determine Q parameter in ARIMA model. then in your code when you call ARIMA why have you used (5,1,0) assuming it is (p,d,q)? i thought it was suppose to be (0,1,5)?

Thanks for the helpful article.

My question is :

“A rolling forecast is required given the dependence on observations in prior time steps for differencing and the AR model.”

can you please elaborate?

How do we decide when to use Rolling forecast and when not to use rolling forecast?

what are the factors do you consider?

Great article! But I have a question. I have a daily time series, and I am following the steps from the time series forecasting book. How do I obtain the acf and pacf visually (for the Manually Congured ARIMA)? because I will have more than 1000 lag values (as my dataset is for many years), and after this I will need to search for the hyperparameters. I will really appreciate the help

However. I have some problem. Whenever I adopt your code for forcasting when no validation data is available, for t in range(93):

model = ARIMA(history, order=(5,1,0))

model_fit = model.fit(disp=0)

output = model_fit.forecast()

yhat = output[0]

predictions.append(yhat)

history.append(yhat)

print('predicted=%f' % (yhat))

my series converge to a constant number after a certain number of iterations, which is not right. What is the mistake?

Your articles are great to read as they give just the right amount of background and detail and are practical oriented. Please continue writing.

I have a question though, being not from the statistical background, i am having difficulty in interpreting the output that is displayed after the summary of the fit model under the heading of “ARIMA model results”. This summarizes the coefficient values used as well as the skill of the fit on the on the in-sample observations.

Can you please provide some explanation on their attributes and how the information assists us in the interpretation of the results

I am training on a dataset where I have to predict Traffic and Revenue during a campaign (weeks 53,54,55) driven by this marketing campaigns. I think I can only use data preceding the campaigns (weeks 1 to 52) even though I have the numbers for campaign and post campaign.

It seems like a statistical problem and I don’t know whether ARIMA is suitable for this use case (very few data, only 52 values to predict the following one). Do you think I can give it a shot with ARIMA or do you think there are other models that could be more suitable for such a use case please?

I am training on a dataset where I have to predict Traffic and Revenue during a campaign (weeks 53,54,55) driven by this marketing campaigns. I think I can only use data preceding the campaigns (weeks 1 to 52) even though I have the numbers for campaign and post campaign.

It seems like a statistical problem and I don’t know whether ARIMA is suitable for this use case (very few data, only 52 values to predict the following one). Do you think I can give it a shot with ARIMA or do you think there are other models that could be more suitable for such a use case please?

Hi Jason, the constant updates are great and very helpful. I need a bit of help with my work. Im trying to forecast solid waste generation in using ANN. But I’m finding challenges with data and modeling my problem. If you could at least get me a headway that can help me produce something in 2weeks I will be grateful. I want to consider variables such as already generated solid waste, population, income levels, educational levels, etc. I hope to hear from you soon.

Just one question, my data set contains some sales value = 0, would that affect the performance of ARIMA model? if there will be issues, anyway I can deal with the zero values in my data set? Thanks in advance for your advice!

Traceback (most recent call last):

File “/Library/Frameworks/Python.framework/Versions/3.7/lib/python3.7/site-packages/pandas/io/parsers.py”, line 3021, in converter

date_parser(*date_cols), errors=’ignore’)

File “/Users/Brian/PycharmProjects/MachineLearningMasteryTimeSeries1/ARIMA.py”, line 9, in parser

return datetime.strptime(‘190’ + x, ‘%Y-%m’)

TypeError: strptime() argument 1 must be str, not numpy.ndarray

During handling of the above exception, another exception occurred:

The formating of csv seems different for everyone who downloads it, here’s the format that is used by Jason (just copy pasted this into a shampoo-sales.csv file and save)

I’m trying to divide time series dataset into several dataset and select the best one as preprocessing dataset.I would like to use RMSE to evaluate each subset.In other word to select the window size and frame size before I do the training . Please let me know if you have any article on rows selection not column selection

Just to clarify my previous question that i have 700 rows of date and price and I would like select the best 70(window size) rows for prediction and decide on the frame size , frame step and extent of prediction.

Please let me know if you have an article help on specifying frame size , frame step and extent of prediction as data pre-processing step using RMSE and SEP.

So I did the for-loop and manage to get different windows.

Now to calculate the RMSE do I need to do linear regiression prediction for each window in order to calculate the RMSE or is there any other way around?

I would expect that you would fit a model for different sized windows and compare the RMSE of the models. The models could be anything you wish, try a few diffrent approaches even.

I got the following as example for two window size 360 days and 180 days

For 360 days

Window start after 0 days with windwo size 360 and step 100 have RMSE 734.1743876097737

Window start after 100 days with windwo size 360 and step 100 have RMSE 369.94549420288877

Window start after 200 days with windwo size 360 and step 100 have RMSE 105.70778076287142

For 180 days

Window start after 0 days with windwo size 180 and step 90 have RMSE 653.9070358902835

Window start after 90 days with windwo size 180 and step 90 have RMSE 326.7832188924093

Window start after 180 days with windwo size 180 and step 90 have RMSE 135.01118940666115

Window start after 270 days with windwo size 180 and step 90 have RMSE 38.422587695965746

Window start after 360 days with windwo size 180 and step 90 have RMSE 60.73374764651785

Window start after 450 days with windwo size 180 and step 90 have RMSE 52.386817309349176

Hey Jason, what model i can use to equipment fault detection and prediction? So have some variables that correlate with others and i need to identification which are. See you soon.

There is something that I struggle to understand, it would awesome if you could give me a hand.

In ARIMA models, the optimization fits the MA and AR parameters. Which can be summed up as parameters of linear combination of previous terms for the AR and previous errors for the MA. A quick math formula could be :

When the fit method is used, it takes the train values of the signal to fit the parameters (a and b)

When the forecast method is used, it forecast the next value of the signal using the fitted model and the train values

When the predict method is used, it forecast the next values of the signal from start to stop.

Let’s say I fit a model on n steps in the train set. Now I want to make predictions. I can predict step n+1. Now I am days n+1 and I have the exact signal value. I would like to actualize the model to predict n+2.

In the rolling forecast part of your code, you fit again the model with the expanded train set (up to n+1). But in that case the model parameters are changed. It’s not the same model anymore.

Is it possible to train one model and then actualize the signal values (the x and e) without changing the parameters (a and b)?

It seems to me that it is important to keep one unique model and evaluate it against different time steps instead of training n different models for each new time steps we get.

I hope I was clear enough. I miss probably a key to understand the problem.

Hi Jason – Very helpful post here, thanks for sharing. I’m curious why parameter ‘p’ should be equal to the number of significant lags from the auto correlation plot? Just was wondering if you could give any more context to this part of the problem. Thanks.

Generally, we want to know how may lag observations have a measurable relationship with the next step so that the model can work on using them effectively.

I used your code to forecast daily temperature (it has a lag of 365). The forecast is always a day behind, i.e. learning history cannot accurately forecast next day’s temperature. I’ve played with the params with AIC.

Thanks for sharing! Very helpful post.

Recently I am writing the methodology of ARIMA, but I can not find any reference (for example, some ARIMA formulas contain constant but some don’t have ). So could you please give me some reference (or ARIMA formula information) of “statsmodels.tsa.arima_model import ARIMA” used in Python?

If one has a time series where the time steps are not uniform, what should be done while fitting a model such as ARIMA? I have price data for a commodity for about 4 years. The prices are available only for days that a purchase was made. This is often, but not always, every day. So sometimes purchases are made after 2, 3 or even more days and the prices are therefore available only for those days I need to forecast the price for the next week.

1. is it necessary that we need to have always uni variate data set to predict for time series using ARIMA? What if i have couple of features that i want to pass along with the date time?

2. is it also necessary that we have a non-stationary data to use time series for modelling? what if the data is already stationary? can i still do the modelling using time series?

Hello sir,

This is a great article. But sir I have couple of questions?

1. Assume that if we have three inputs and one output with time period. Then how do we predict the next future value according to the past values to next time period using ARIMA model? (if we need to predict value next time interval period is 120min)

as a example

You could treat the other inputs as exogenous variables and use ARIMAX, or you could use another method like a machine learning algorithm or neural network that supports multivariate inputs.

I was wondering if you are aware of any auto arima functions to fine tune p,d,q parameters. I am aware that R has an auto.arima function to fine tune those parameters but was wondering if you’re familiar with any Python library.

Have followed your post : “How to Grid Search ARIMA Model Hyperparameters with Python” to fine tune the p,q and d value. Have come across the below point in the post.

“The first is to ensure the input data are floating point values (as opposed to integers or strings), as this can cause the ARIMA procedure to fail.”

My initial data is in the below format. Month and #Sales

With this log value, applied the grid search approach to decide the best value of p,q and d.

Howver, I got Best ARIMA(0, 1, 0) MSE=0.023. Looks good ? is it acceptable? Wondering if p=0 and q=0 is acceptable. Please confirm.

Next, I have 37 Observations from Nov 2014 to 31-Dec-2017. I want to do future predictions for 2018, 2019 etc.How to do this?

Also, do you have any Youtube videos explaining each of the steps in grid approach, how to make future forecatsts available ? It would be great if you can share the Youtube link. 🙂

Once again thanks a lot for the article and your help!

Kindly confirm if the p,q value is 0 is an acceptable scenario.

Perhaps try standardizing or normalizing the data as well : I am not sure how to proceed with this?

It would be great if you can share related article if you have any. 🙂

For now, I am going to implement the future forecasting using the above link with this ARIMA(0,1,0) and will check how it behaves. 🙂

Hi Jason, thanks for the tutorial i am new to the world of predictive analysis but i have a project to predict when a customer is likely to make next purchase. I have dataset which include historical transactions and amount.

Will this tutorial help me or is there any suggestion on material/resource i can use.

Used your epic tutorial to forecast bookings.

I used the whole of 2017 as my data set and after applying everything in your post the predicted graph seems to be one day off i.e. prediction graph looks spot on with each data point very close to the what it should be, the only thing is is that it’s a day late…is this normal? Is there something within the code that causes something like this?

Hi, i have had a question for a while, now this might be silly but I can’t figure out whats wrong here…

So I have a timeseries data and when i used order=(0,1,0) that is, differencing is 1 then i get a timeseries that is ahead of time by one.

example:

input: 10, 12, 11, 15

output: 8, 9.9, 12.02, 11.3, 14.9

Now if I shift the resulting series by one timeperiod, it’ll match quite well.

Also, similar output can be seen is (0,2,1) that is, differencing is 2 and MA is 1.

Could someone explain why is this happening and what am i missing here.

[numbers in example are representative not actual]

Thanks Jason, I went through the link and it helps me see a clear picture which should have been obvious to notice but i missed it.

If you please, could also share some thoughts on…

– My model uses order(0,1,0). i.e. differencing is 1. Do such model makes sense for a practical scenario where we are trying to predict inventory requirement for a part(based on past consumption) that may fail in coming future(where failing of a part is totally a random act of nature).

– Also, (0,2,1) and (0,1,0) gives very similar results. Is this expected in some sense. Is there any concept that i am missing here.

Thank you for the tutorial. It’s a good start to implementing an ARIMA model in Python. I have a question: You have used the actual data samples to update your training dataset after each prediction as given in “history.append(obs)”. Now let’s take a real life example when you don’t have any further actual data and you use your predictions only to update your training dataset which looks like “history.append(yhat)”. What will happen in this case? I am working on air quality prediction and in my case, the former scenario keeps the seasonal pattern in the test set but the latter does not show any seasonal pattern at all. Please let me know what’s your take on this.

Hi Jason ,

Thank you for the tutorial.

I have two questions :

first : why you set moving average “q” Parameter by 0 ?

second : why you set Lag value To 5 not 7 for example?

Thanks.

I know that the third output from model_fit.forecast() consists of the confidence interval. But how can I plot the confidence interval on the whole range automatically?

I’m running this with a separate data set. I’ve shaped my dataset, but when I run the error line, I’m getting this:

ValueError: Found array with dim 3. Estimator expected <= 2.

Code:

history = [x for x in X_train]

predictions = list()

for t in range(len(X_test)):

model = ARIMA(history, order=(10,0,3))

model_fit = model.fit(disp=0)

output = model_fit.forecast()

yhat = output[0]

predictions.append(yhat)

obs = X_test[t]

history.append(obs)

print('predicted=%f, expected=%f' % (yhat, obs))

Hi Jason,

Thanks for this great work!

If you allow me, I have a question: how was the confidence interval calculated in the above example? I know its equation, but I do not know what are the values to be used for (sigma) and (number of samples).

Thank you once more.

Thanks a lot Jason!

I am preparing a time series model for my capstone project, i have around 500 items and the p,d,q value is different for each item, how can i deploy this as a tool? do i have to create model each time for different items?

How many minimum data points do we require for creating accurate prediction using ARIMA model. We are predicting future cut-off values of colleges using previous records, how many years of records would we need to predict just the cutoff value of next year.

Hi Jason Brownlee!

I have been following your blog since some time and the concepts and code snippets here often come handy.

I’m totally new to time series analysis and have read some posts (mostly yours), a few lectures and of course questions from stackoverflow.

What confuses me is, to make a series stationary we difference it, double differencing in case seasonality and trend both are present in the series. Now while performing ARIMA, the parameter ‘I’ depicts what? Number of times we have performed differencing or lag value we chose for differencing (for the removal of seasonality).

For example, let say there is a dataset of monthly average temperatures of a place (possibly affected by global warming). Now there is seasonality (lag value of 12) and a global upward trend too.

before performing ARIMA I need to make the series stationary, right?

To do that I Difference twice like this:

differenced = series – series.shift(1) # to remove trend